The Tax Reform, regulated by LC 214/2025, is rewriting the rules of the fiscal game in Brazil. At the heart of this transformation, for the service sector, is the rise of the Brazilian Service Classification (NBS).

Created over a decade ago, the NBS, which classifies services in detail (similar to what the NCM does with products), is no longer a one-off reference and has become the central element for identifying and calculating new taxes: the IBS (Tax on Goods and Services) and the CBS (Contribution on Goods and Services), which will replace the ISS and PIS/COFINS.

From now on, the correct classification of your service in the NBS will be the determining factor for the tax rate, the calculation regime, and the application of tax benefits. Ignoring this transition is tantamount to assuming a high risk of fines and loss of credits.

The critical impact of NBS on SAP environments

If your company uses SAP, NBS represents an immediate compliance project that goes far beyond updating a table. It requires a thorough review of your ERP's data architecture and tax rules.

Why does NBS require immediate attention in SAP?

1. Apuração de IBS e CBS: Os novos tributos serão calculados com base na classificação do serviço pela NBS. Se seu cadastro de serviços (e a parametrização fiscal associada) estiver incorreto no SAP, o cálculo dos impostos na emissão e recebimento de notas estará errado.

2. Benefícios Fiscais e Regimes Especiais: Eventuais reduções de base de cálculo, alíquotas diferenciadas e regimes especiais serão aplicados com base nos códigos da NBS. Se o seu SAP não souber identificar o serviço corretamente pela nova nomenclatura, sua empresa pode perder benefícios legítimos.

3. Risco de Autuação e Glosas: A divergência entre o que seu sistema informa e o que o Fisco exige, balizado pela NBS, pode gerar glosas de crédito e autuações, comprometendo a saúde financeira e jurídica da empresa.

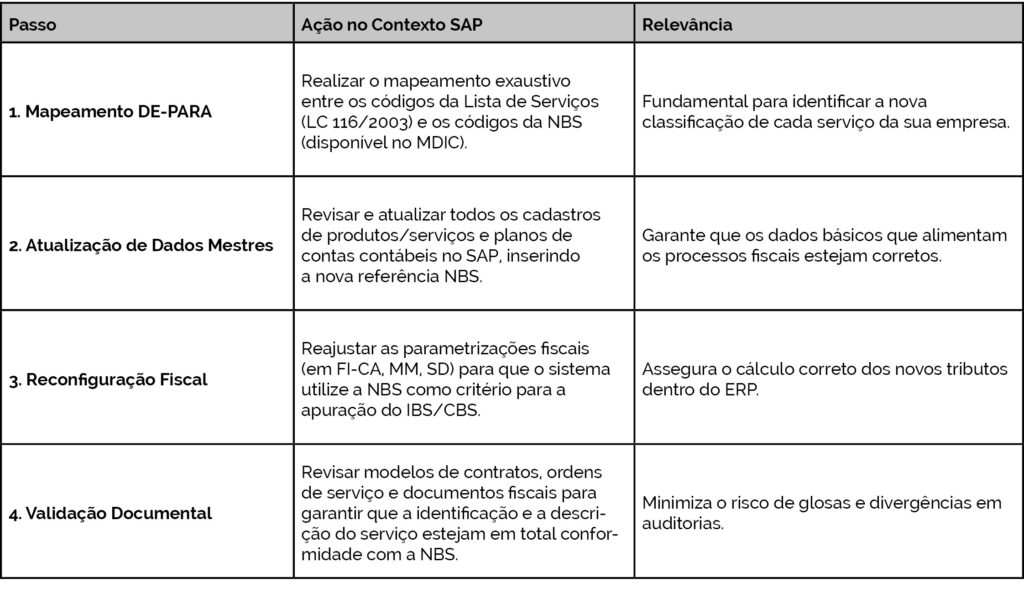

4. Ajuste de Cadastros e Tax Procedures: O sistema SAP precisa ser configurado para que os módulos de Vendas, Compras e Contabilidade usem a NBS como chave primária na determinação fiscal. Isso exige um trabalho meticuloso de mapeamento DE-PARA e reconfiguração das Tax Procedures.

The transition from the old List of Services under LC 116/2003 to the NBS is not a technical adjustment, but an essential measure for fiscal governance in the new model.

The 4 practical steps to prepare your SAP

To ensure that your SAP environment is prepared, we recommend focusing on these steps:

Don't wait to be notified by the tax authorities. Companies that anticipate and adjust their systems now ensure greater legal certainty and predictability in the new tax environment.

Talk to CVA. Turn the complexity of tax reform into a strategic advantage for your business.

Follow us on social media: